You are engaging in a process to benchmark plan level fees by service category. To determine if fees are reasonable the Department of Labor (DOL), the Courts, as well as many law firms, suggest a comparative process. A comparative process could involve either a formal Request for Information/Proposal (RFI/RFP) or benchmarking. Neither approach is mandated by statute or regulation but both are preferred methods of proving a documented process does exist. Failure to establish a documented process leaves a fiduciary vulnerable in a claim of fiduciary breach. Between the two options, conducting a formal RFI/RFP is the most time consuming and expensive. This may be why some Courts have suggested this process be pursued once every 3 to 5 years. FRA PlanTools™ does offer a RFI/RFP solution to assist with a search for a qualified advisor. The process follows court room standards for determining an advisor’s level of expertise. The cost is $995. For more information on this solution click here.

Alternatively, or at least in years an RFI/RFP is not conducted, benchmarking fees by service category is a time and cost efficient method of monitoring fees. It is important to emphasize that assessing fee reasonableness is not a one and done approach. A fiduciary is expected to monitor fees on a continuous basis. Changes in technology, investment options, share classes, revenue sharing terms, participant count, asset values, regulations and the benchmarking database all influence the determination of fee reasonableness. As such, it behooves a fiduciary to analyze and monitor fees at least annually to establish a process exists to determine fee reasonableness. However, benchmarking is only 1 of a 3 STEP process to comply with ERISA 408(b)(2).

ERISA 408(b)(2) imposes 3 STEPS to secure the exemption from a prohibited transaction when paying fees from plan assets. Remember, the DOL does not care if the company pays excessive fees from company assets but the DOL is intolerant of a plan paying excessive fees. For purposes of complying with ERISA 408(b)(2), the 3 STEPS are as follows:

- CONFIRM: You must confirm three things:

- The Plan Document permits the payment of fees from plan assets,

- The services are necessary for the establishment and/or operation of the plan, and

- The expense is not for settlor services.

- EVALUATE: Once you confirm it is a permissible fee that may be deducted from plan assets you must evaluate fees to determine if they are reasonable. This includes:

- Evaluate reasonableness for each service component – evaluating fees for the plan in aggregate is not acceptable!

- Evaluate reasonableness for services rendered – Assuming all else is equal, the service provider that does more for less is the most prudent choice; however, quantity should not be considered in a vacuum. In addition to quantity, you need to consider quality and value, both are subjectively assessed; therefore, we suggest that you document your conclusions as to why you believe your choice is preferable based on quantity, quality and value.

- Evaluate revenue sharing – If indirect revenue sharing is a source of compensation to any service provider, the Courts are looking for proof you have converted the amount to dollars and compared it to other revenue sharing platforms. Not all platforms are the same, so a comparative analysis is a must to determine if the amount of indirect fees are reasonable.

- VALIDATE: This is the most difficult STEP for a plan sponsor. Validating requires a comparison of the fee disclosures received to the regulations to confirm the disclosures are complete. Failure to validate disclosures are complete leaves the plan sponsor susceptible to monetary damages if a fiduciary breach claim is filed and it is discovered that no assessment has been conducted. Unfortunately few plan sponsors have the skill, knowledge and experience necessary to process a comprehensive assessment. To assist you in this endeavor, we offer the following solutions:

- Your options if you are a Plan Sponsor or a Service Provider:

- You DO IT: You provide us with a copy of your disclosures and we create a custom checklist for each service provider for your use to validate compliance.

- We ASSIST: You provide the disclosures; we create the custom checklist and review your analysis.

- We DO IT: You provide us with your disclosures and we prepare the analysis.

Cost for creating a custom checklist is $750. Additional fees apply if we assist or do the analysis for you. To request a consultation to discuss, click here.

- Call for a referral – If you prefer a referral to an independent fee-for-service consultant in your region to assist or conduct the analysis click here.

- Select an Advisor – Alternatively, you can visit the Community Center to conduct your own search. The Community Center provides you with advisors in your region. The profile is a helpful tool that will assist you in evaluating the options. As a subscriber you have access to the Community Center for no additional charge. Advisory fees for conducting the analysis will be disclosed by the advisor.COMING SOON!

It may be possible to deduct the cost of benchmarking from plan assets if the plan document permits the deduction of such expenses, the expense is considered necessary for the operation of the plan and the expense is reasonable. ERISA also includes a provision that will enable you to seek reimbursement from the plan if you pay the expense. However, before deducting any expense from plan assets you should seek the opinion of ERISA counsel.

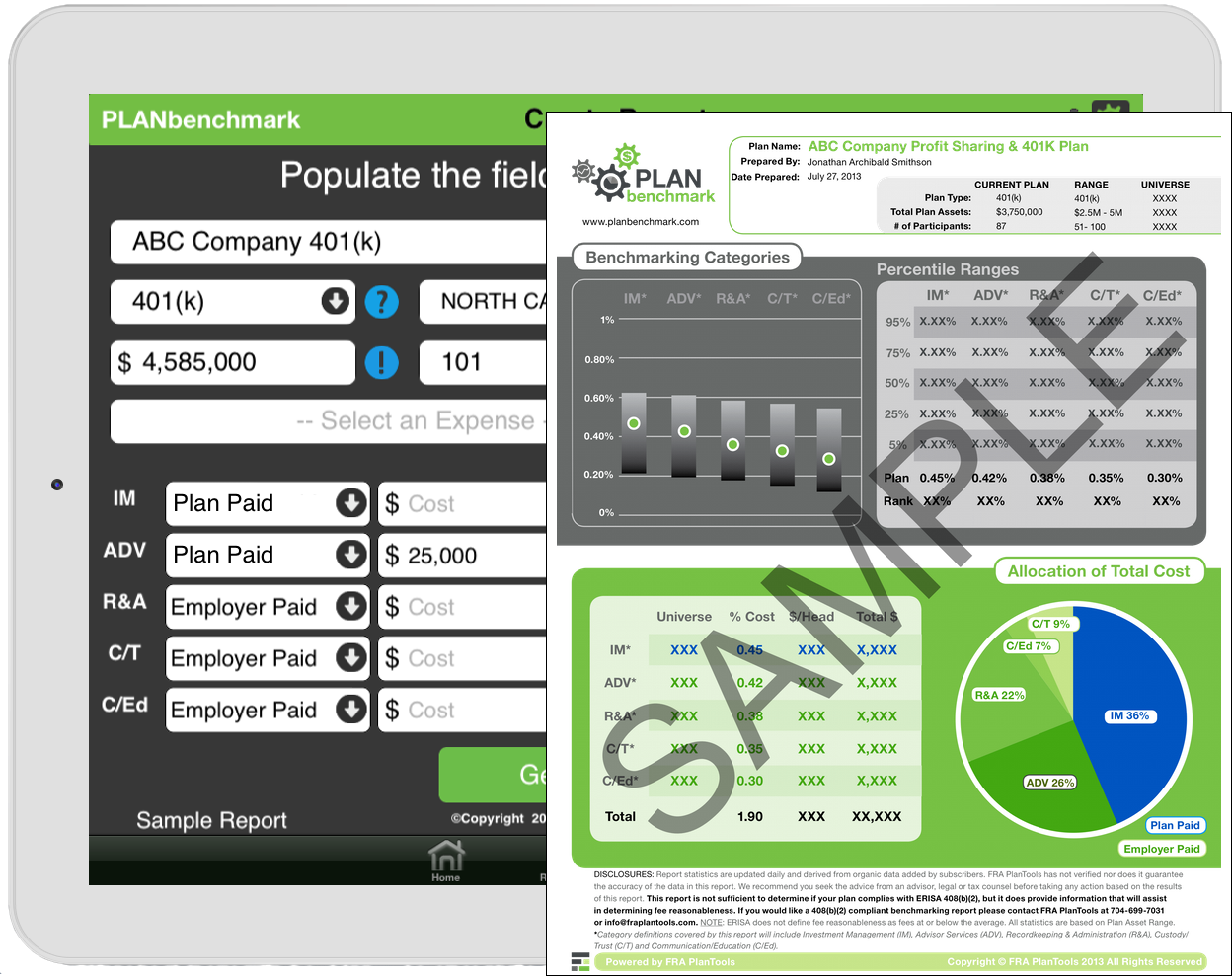

To see a sample of the report, Download the App for free.